Downloaded 29 times

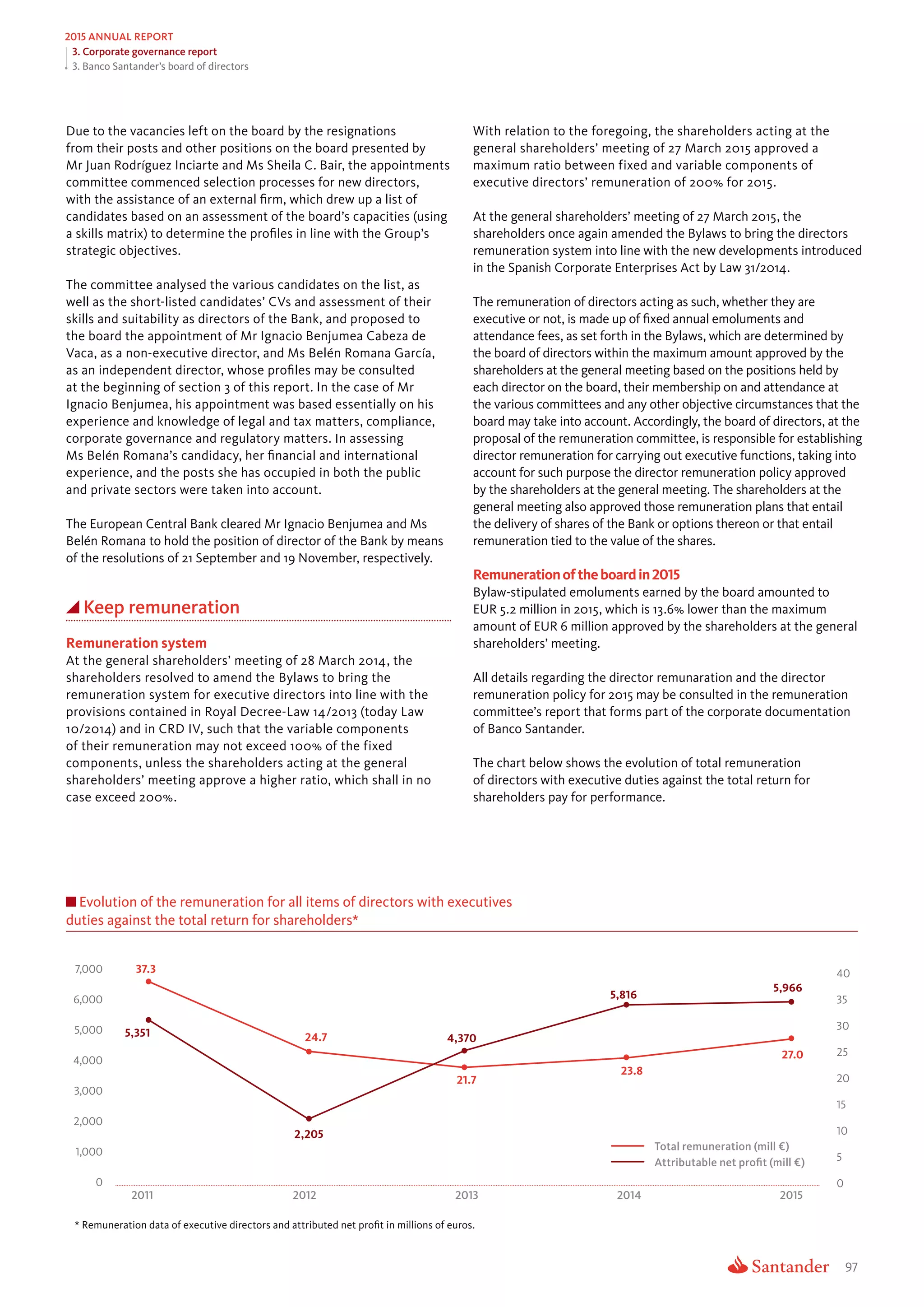

![194

Background and upcoming challenges

Risk management report

2015 Annual report

• Publication by the European Banking Authority (EBA) of the results

of the transparency exercise, a preliminary step before the stress

tests to be held in 2016.

• Entities’ progress in projects designed to address regulatory

changes regarding provisions, to come into force from 2018 on

according to the IFRS 9 standard [refer to details in Table 1].

Regulatory compliance is a priority for Grupo Santander, and as such

the Group constantly keeps track of new regulatory developments.

Particularly worthy of note in 2015 were the steps forward taken in

developments designed to satisfy the requirements of the Volcker

rule (further details in section 3. Market regulations, section

D.5.4. Regulatory compliance) and international standards on risk

data aggregation (RDA) (further details in section B.3.5. Risk Data

Aggregation Risk Reporting Framework).

From the supervisory standpoint, 2015 marks one year since the

coming into force of the Single Supervisory Mechanism (SSM).

Supervisory activity by Eurozone banking entities has been

conducted through the joint supervisory teams (JST) and through

common ongoing supervision which includes the methodology

known as the Supervisory Review and Evaluation Procedure (SREP3

).

This methodology is based on four key areas:

a. Analysis of business model;

b. Assessment of internal governance and global controls;

c. Assessment of capital risks; and

d. Assessment of liquidity risks.

Growth in the global economy slowed in 2015 because the steady

resurgence in developed countries, which has been more vigorous

in the US and the United Kingdom but also in the Eurozone, was

significantly offset by the downturn in emerging markets.

Growth has been lower than was expected at the start of the year.

In developed economies, this has been the case due to specific

circumstances which dragged on the US economy in early 2015, even

though by December this did not stop the FED from implementing a

slight rise in interest rates. In the Eurozone, the year saw moderate

improvement until Greece’s third bail-out and the point at which

the ECB began to apply a more active policy (quantitative earing).

Emerging countries have been impacted by the slowdown in China

(and the change in China’s growth mix), the fall in commodity prices,

geopolitical problems and some measure of decline in financing

conditions (lower capital outflows, rise in risk premiums, stock

market falls).

Against this background, Banco Santander has a medium-low risk

profile, with improved credit quality as evidenced by its core ratios:

NPL ratio of 4.36% (- 83 b.p. vs. December 2014), cost of credit 1.25%

(-18 b.p. vs. December 2014 ) and a coverage ratio of 73% (+6 p.p

higher than in December 2014).

During 2015, the regulatory background has once again been

shaped by highly demanding prudential requirements. These are

some of the highlights which have happened this year:

• The BCBS’s review of the initial proposals for credit, market and

operational risk prudential frameworks.

• Regulatory progress concerning loss absorption mechanisms in the

event of resolution situations (MREL and TLAC).

EXECUTIVE SUMMARY

A. PILLARS OF THE RISK FUNCTION

B. RISK CONTROL AND MANAGEMENT MODEL - Advanced Risk Management

C. Background and upcoming challenges

D. RISK PROFILE

APPENDIX: EDTF TRANSPARENCY

C. Background and

upcoming challenges

3. According to the document published by the European Banking Authority (EBA): Guidelines on common procedures and methodologies for the supervisory review and evaluation

process (SREP)](https://image.slidesharecdn.com/annual-report-2015-160215092003/75/Annual-report-2015-Banco-Santander-194-2048.jpg)

![199

Risk profile Credit risk

Risk management report

2015 Annual report

• The segment of SMEs, companies and institutions includes

companies and physical persons with business activity. It also

includes public sector activities in general and non-profit making

private sector entities.

• The segment of Santander Global Corporate Banking – SGCB –

consists of corporate clients, financial institutions and sovereigns,

who comprise a closed list revised annually. This list is determined

on the basis of a full analysis of the company (business, countries

where it operates, types of product used, volume of revenues it

represents for the bank, length of relation with the client, etc.).

The following chart shows the distribution of credit risk on the basis

of the management model.

Credit risk distribution

Individuals

57%

SMEs, companies

and institutions

27%

SGCB

16%

The Group’s profile is mainly retail, accounting for 84% of total risk

generated by the retail banking business.

Organisation of this section

After an introduction to the concept of credit risk and the

segmentation that the Group uses for its treatment, the key figures

of 2015 and change over time are presented [pag. 200-207].

This is followed by a look at the main geographies, setting out the

main features from the credit risk standpoint [pag. 208-215].

The qualitative and quantitative aspects of other credit risk matters

are then presented, including information on financial markets, risk

concentration, country risk, sovereign risk and environmental risk

[pag. 216-224].

Lastly, there is a description of the Group’s credit risk cycle, with

a detailed explanation of the various stages that form part of the

phases of pre-sale, sale, and post-sale, as well as the main credit risk

metrics [pag. 224-229].

D.1.1. Introduction to credit risk treatment

Credit risk arises from the possibility of losses stemming from the

failure of clients or counterparties to meet their financial obligations

with the Group.

The Group’s risks function is organised on the basis of three types of

customers:

• The segment of individuals includes all physical persons, except

those with a business activity. This segment, in turn, is divided into

sub segments by income levels, which enables risk management

adjusted to the type of client.

D.1. Credit risk

D. Risk profile

EXECUTIVE SUMMARY

A. PILLARS OF THE RISK FUNCTION

B. RISK CONTROL AND MANAGEMENT MODEL - Advanced Risk Management

C. BACKGROUND AND UPCOMING CHALLENGES

D. D. RISK PROFILE

1. Credit risk

2. Trading market risk and structural risks

3. Liquidity risk and funding

4. Operational risk

5. Compliance and conduct risk

6. Model risk

7. Strategic risk

8. Capital risk

APPENDIX: EDTF TRANSPARENCY](https://image.slidesharecdn.com/annual-report-2015-160215092003/75/Annual-report-2015-Banco-Santander-199-2048.jpg)

![250

Risk profile Liquidity risk and funding

Risk management report

2015 annual report

The Group adopts a decentralised funding model, based on

autonomous subsidiaries that are self-sufficient in their liquidity

needs. Each subsidiary is responsible for covering the liquidity

needs of its current and future activity, either through deposits

captured from its customers in its area of influence or through

recourse to the wholesale markets in which it operates, within

a management and supervision framework coordinated at the

Group level.

The funding structure has shown its great effectiveness in

situations of high levels of market stress, as it prevents the

difficulties of one area from affecting the funding capacity of other

areas, and thus of the Group as a whole, as could happen in the

case of a centralised funding model.

Moreover, at Grupo Santander this funding structure benefits

from the advantages of a solid retail banking model with a

significant presence in ten high potential markets, focused on

retail clients and high efficiency. All of this gives our subsidiaries

substantial capacity to attract stable deposits, as well as a strong

issuance capacity in the wholesale markets of these countries,

generally in their own currency, backed by the strength of their

franchise and belonging to a leading group.

D.3.2. Liquidity management

Management of structural liquidity aims to fund the Group’s

recurring activity in optimum conditions of maturity and cost,

avoiding the assumption of undesired liquidity risks.

Santander’s liquidity management is based on the following principles:

• Decentralised liquidity model.

• Needs derived from medium- and long-term activity must be

financed by medium- and long -term instruments.

• High contribution from customer deposits, derived from the

retail nature of the balance sheet.

• Diversification of wholesale funding sources by instruments/

investors, markets/currencies and terms.

• Limited recourse to wholesale short-term funding.

Structure of this section

Following an introduction to the concept of liquidity risk and

funding in Grupo Santander [pag. 250], we present the liquidity

management framework put in place by the Group, including

monitoring and control of liquidity risk [pag. 250-254].

We then look at the funding strategy developed by the Group

and its subsidiaries over the last few years [pag. 254-256],

with particular attention to the evolution of liquidity in

2015. For the last year, we examine changes in the liquidity

management ratios and the business and market trends that gave

rise to these [pag. 256-260].

The section ends with a qualitative description of the prospects

for funding for the next year for the Group and its main countries

[pag. 260].

D.3.1. Introduction to the treatment

of liquidity risk and funding

• Santander has developed a funding model based on autonomous

subsidiaries responsible for covering their own liquidity needs.

• This structure makes it possible for Santander to take advantage

of its solid retail banking business model in order to maintain

comfortable liquidity positions at Group level and in its main

units, even during stress in the markets.

• In the last few years, as a result of the economic and regulatory changes

arising from the global economic and financial crisis, it has been

necessary to adapt the funding strategies to new commercial business

trends, market conditions and new regulatory requirements.

• In 2015, Santander continued to improve in specific aspects

based on a very comfortable liquidity position at the level of

the Group and in the subsidiaries, with no significant changes

in liquidity management or funding policies or practices. All of

this enables us to face 2016 from a good starting point, with no

restrictions on growth.

Liquidity management and funding have always been basic elements

in Banco Santander’s business strategy and a fundamental pillar,

together with capital, in supporting its balance sheet strength.

D.3. Liquidity risk and funding](https://image.slidesharecdn.com/annual-report-2015-160215092003/75/Annual-report-2015-Banco-Santander-250-2048.jpg)

![281

Risk Profile Capital risk

Risk management report

2015 Annual report

At 31 December 2015, the Group’s main capital ratios are as follows:

Fully loaded Phase-in

Common Equity (CET1) 10.05% 12.55%

Tier1 11.00% 12.55%

Total Ratio 13.05% 14.40%

Leverage ratio 4.73% 5.38%

Phase-in ratios are calculated applying the transitional Basel III implementation

schedules, while Fully loaded ratios are calculated using the final standard.

On 3 February, 2016, the European Central Bank authorised the use

of the Alternative Standard Method to calculate capital requirements

at consolidated level for operational risk in Banco Santander (Brasil)

S.A. The impact of this authorization on the Group’s risk-weighted

assets (-EUR 7,836 million), and, consequently, on its capital ratios,

has not been taken into account in the data published on 27 January

and which are presented in this report.

At the end of 2015, the ECB sent every entity a notification setting

out the minimum prudential capital requirements for the following

year. For 2016, Grupo Santander must maintain a minimum phase-

in CET1 capital ratio at the consolidated level of 9.75% (9.5% being

the Pillar I, Pillar II and capital buffer requirements and 0.25% the

requirement for being a Systemically Important Financial Institution).

As can be seen from the table above, the Group’s capital exceeds the

ECB’s minimum requirement.

14.4%

9.75%

Regulatory capital

%

Regulatory requirement1

2016 CET1

Regulatory ratios

Dec 15

1. Minimum prudential requirements established by the ECB based on the

supervisory review and assessment process (SREP)

Capital

ratio

CET1

CET1

Systemic buffer

Minimum Pillar I4.50

5.00

0.25

Pillar II requirement

(including capital

conservation buffer)

12.55

The Group is working towards its goal of having a CET1 fully loaded

of more than 11% by 2018.

Organisation of this section

After an introduction to the concept of capital risk and solvency

levels at the close of 2015, the key capital figures are outline (pag.

pag.281-282].

Next we describe the regulatory framework from a capital

standpoint [pag. 282-283].

After that, the regulatory capital and economic capital figures are

presented [pag. 283-287].

Lastly, we describe the capital planning process and stress tests in

Grupo Santander [pag. 287-289].

For further details, refer to the Prudential Risk Report of Grupo

Santander (Pillar III).

D.8.1. Introduction

Santander defines capital risk as the risk that the Group or some of

its companies do not have the amount and/or quality of sufficient

equity to meet the minimum regulatory requirements set for

operating as a bank, to fulfil on the market’s expectations about its/

their credit solvency and support business growth and the strategic

possibilities they present, in accordance with the strategic plan. Of

note are the following objectives:

• complying with the internal objectives for capital and solvency.

• meeting regulatory requirements.

• aligning the Bank’s strategic plan with the capital expectations

of outside agents (rating agencies, shareholders and investors,

customers, supervisors, etc.)

• supporting the growth of the businesses and exploit the strategic

opportunities that arise.

Grupo Santander has a comfortable solvency position, above the

levels required by regulators and by the European Central bank, our

supervisor. In 2015, the Group continued to bolster its capital ratios

in view of the adverse economic setting and to comply with new

regulatory requirements. In early 2015, it carried out a EUR 7.5 billion

accelerated book building operation, and established a dividend

policy which assures organic capital generation.

D.8. Capital risk](https://image.slidesharecdn.com/annual-report-2015-160215092003/75/Annual-report-2015-Banco-Santander-281-2048.jpg)

- Santander delivered strong results in 2015, growing earnings, dividends, and capital organically. However, its share price has fallen, partly due to concerns over emerging markets like Brazil. - Santander is well capitalized with a CET1 ratio of 12.55%, far above its minimum requirements, to prepare for Basel III standards. Its diversified business model provides stable earnings through economic cycles. - Santander has a "moat" of competitive advantages including critical mass across its markets, trusted customer relationships, and geographic diversification that help protect its profits and market share over time.

![Current State of Fast-Casual Franchises [Appraisal Economics]](https://cdn.slidesharecdn.com/ss_thumbnails/current-state-of-fast-casual-franchises-appraisal-economics-10-28-20250151am-251027202229-ae80bc1e-thumbnail.jpg?width=640&height=640&fit=bounds)