FutureNow Understanding the Nigerian Tax System and the Implications of the New Reforms on SMEs - Prof Oyedokun .pptx

1.

Understanding the NigerianTax System and the Implications

of the New Reforms on SMEs

Prof. Godwin Emmanuel Oyedokun

Professor of Accounting and Financial Development

Department of Management & Accounting

Faculty of Management and Social Sciences

Lead City University, Ibadan, Nigeria

Principal Partner; Oyedokun Godwin Emmanuel & Co

(Accountants, Tax Practitioners & Forensic Auditors)

Being a Paper Presented at the Future Now Africa Webinar Series on Sunday, February 16, 2025.

2.

ND (Fin), HND(Acct.), BSc. (Acct. Ed), BSc (Fin.), LLB., LLM, MBA (Acct. & Fin.), MSc. (Acct.), MSc. (Bus &Econs), MSc. (Fin), MSc.

(Econs), Ph.D. (Acct), Ph.D. (Fin), Ph.D. (FA), CICA, CFA, CFE, CIPFA, CPFA, CertIFR, ACS, ACIS, ACIArb, ACAMS, ABR, IPA, IFA,

MNIM, FCA, FCTI, FCIB, FCNA, FCFIP, FCE, FERP, FFAR, FPD-CR, FSEAN, FNIOAIM, FCCrFA, FCCFI, FICA, FCECFI, JP

Prof. Godwin Emmanuel Oyedokun

Professor of Accounting and Financial Development

Department of Management & Accounting

Faculty of Management and Social Sciences

Lead City University, Ibadan, Nigeria

Principal Partner; Oyedokun Godwin Emmanuel & Co

(Accountants, Tax Practitioners & Forensic Auditors)

Contents

Introduction

The Nigerian Tax

System

Legaland

Regulatory

Framework

Structure of the

Nigerian Tax

System

Challenges of the

Nigerian Tax

System

The New Proposed

Tax Bill in Nigeria

Objectives and

Rationale

Tax Incentives for

Business Growth

and Investment

Changes to

Personal Income

Taxes

Personal Income

Tax (PIT) Structure

VAT and

Consumption Taxes

Disparities in VAT

Contribution and

Allocation

Impact on MSMEs

and Startups

Implications of

New Tax Laws for

Individuals and

Businesses

Tax Provisions for

Businesses in

Nigeria

Personal Income

Tax (PIT) Filing for

Individuals

Companies Income

Tax (CIT) Filing for

LLCs and

Corporations

Effect of WHT on

SMEs &

Consultancy Firms

Effect of VAT on

SMEs and

Consultancy

Businesses

Conclusion

5.

Introduction

The Nigerian taxsystem is a critical component of the country's

economic framework, serving as a key revenue source for government

operations and national development. Taxation plays a fundamental

role in wealth redistribution, economic stability, and public service

funding.

Small and Medium Enterprises (SMEs) constitute a significant portion of

Nigeria’s economy, contributing approximately 48% of the national GDP

and accounting for over 84% of employment in the country. The recent

tax reforms aim to improve tax administration, increase government

revenue, and create a more favorable business environment.

6.

The Nigerian TaxSystem

Economic Growth

The Nigerian tax system is a structured framework for

revenue generation designed to support economic growth,

public infrastructure, and social services.

Fiscal Federalism

It is governed by various laws, policies, and regulatory

agencies at the federal, state, and local levels. The system is

based on the principle of fiscal federalism.

7.

Legal and Regulatory

Framework

1Constitution

The Constitution of the

Federal Republic of Nigeria

(1999, as amended)

provides the legal basis for

taxation powers.

2 FIRS Act

The Federal Inland Revenue

Service (FIRS) Act (2007)

establishes and empowers

FIRS to administer federal

taxes.

3 Companies Income Tax Act

The Companies Income Tax Act (CITA) governs taxation of

corporate entities.

8.

Structure of theNigerian

Tax System

Federal Taxes

Administered by FIRS,

including Companies Income

Tax (CIT) and Value Added Tax

(VAT).

State Taxes

Administered by State Internal

Revenue Services (SIRS),

including Personal Income Tax

(PIT).

Local Taxes

Local Government Taxes and Levies, including Tenement Rates and

Market Taxes.

9.

Challenges of theNigerian

Tax System

Tax Evasion

High levels of

informal sector

activities make

enforcement difficult.

Multiple

Taxation

Businesses often face

overlapping tax

burdens from

different government

levels.

Low Tax-to-GDP

Nigeria's tax revenue

as a percentage of

GDP remains low

compared to global

standards.

10.

The New ProposedTax Bill

in Nigeria

Nigeria Tax Bill 2024

Seeks to provide a comprehensive fiscal framework for

taxation, harmonizing major taxes into a single legislation.

Tax Administration Bill

Aims to reduce disputes and enhance compliance by

providing streamlined tax administration procedures.

Nigeria Revenue Service Establishment Bill

Intended to strengthen tax collection and administration.

4

Joint Revenue Board Establishment Bill

Aimed at creating a tax tribunal and a tax ombudsman, this

bill seeks to harmonize, coordinate, and resolve disputes

arising from revenue administration in Nigeria.

11.

Objectives and Rationale

ProgressiveTaxation

The tax system aims to be more progressive, ensuring

that higher-income earners and large corporations pay

a fair share of taxes.

Protecting Low-Income Earners

The bill includes provisions for protecting low-

income earners, such as tax credits and exemptions

for basic necessities.

Boost Revenue

To increase government revenue for critical infrastructure

projects, social programs, and economic development.

Enhancing Tax Compliance

The bill aims to increase tax revenue by expanding the

tax base and ensuring that more individuals and

businesses contribute to national development.

Modernizing the Tax System

The bill seeks to introduce digital tools for tracking and

collecting taxes, streamline tax processes, and reduce

bureaucratic inefficiencies.

12.

Objectives and

Rationale

Tax Incentives

Thebill encourages both local and foreign

investment, especially in sectors such as

manufacturing, technology, and renewable

energy.

Stimulating Business Growth

These provisions are designed to stimulate

business growth, create jobs, and foster

entrepreneurship, particularly in the formal and

informal sectors.

Broaden Tax Base

To expand the tax base by capturing previously

untaxed income and activities, including the informal

sector.

13.

Tax Incentives forBusiness Growth and

Investment

R&D Tax Credits

The bill proposes a 15% tax credit for businesses investing

in R&D, especially leading to new products or services. This

incentive is aimed at promoting innovation, improving

productivity, and bolstering industries that can create jobs

and stimulate the economy.

Tax Relief for Strategic Sectors

The bill provides tax incentives such as investment

allowances, exemptions, and credits for specific sectors,

including renewable energy, agriculture, and technology.

These incentives are designed to attract both domestic and

international investment, propel sectoral growth, and

reduce Nigeria’s reliance on oil revenue.

14.

Changes to Personal

IncomeTaxes

1 Tax Brackets

Introducing revised tax

brackets to make the

system more progressive

and ensure fairness.

2 Tax Relief

Expanding tax relief

provisions for low-income

earners and individuals

with dependents to

alleviate the tax burden.

15.

Personal Income Tax(PIT) Structure

1

₦800,000

0%

2

₦2,200,000

15%

3

₦9,000,000

18%

4

₦13,000,000

21%

5

₦25,000,000

23%

16.

The Current VATSharing

Formula: A Breakdown

50%

Equality

A 50% share is allocated equally to all

states, regardless of their contributions

or population.

30%

Population

A 30% share is distributed based on

population, favoring states with larger

populations.

20%

Derivation

A 20% share is allocated based on the

derivation principle, rewarding states

with natural resources.

17.

The Proposed NewVAT Sharing Formula

1

Derivation

60%

2

Population

20%

3 Equality

20%

The proposed formula prioritizes derivation, allocating 60% based on natural resources while the Nigerian Governors’ Forum

(NGF) proposed 30% based on derivation. This change aims to incentivize resource-rich states to contribute to national

development while ensuring that they receive a greater share of the revenue generated from their resources.

1

2

3

Derivation

30%

Population

20%

Equality

50%

Proposed New Tax Bill Governors’ Forum Proposal

18.

18

Geopolitical Zones andVAT Pool

1 SOUTH WEST

Contributed: N3.11trn

Received: N849.71bn (27.4%)

2 SOUTH SOUTH

Contributed: N1.08trn

Received: N543.49bn (50.3%)

3 NORTH WEST

Contributed: N211.27bn

Received: N574.32bn (271.8%)

4 NORTH EAST

Contributed: N174.50bn

Received: N411.84bn (236%)

5 NORTH CENTRAL

Contributed: N154.54bn

Received: N408.66bn (264.4%)

6 SOUTH EAST

Contributed: N101.09bn

Received: N341.46bn (337.8%)

19.

VAT and ConsumptionTaxes

Adjusted VAT Rates

The bill suggests raising VAT rates on luxury goods while

offering lower VAT rates or exemptions for essential items

such as food and medicine. This approach aims to balance

tax revenue generation with protecting lower-income

earners from excessive consumption taxes.

Digital Service Consumption Tax

Following global trends, the bill introduces VAT on digital

services provided by foreign companies, including

streaming services, e-commerce, and online platforms. This

ensures that digital companies operating in Nigeria

contribute to the tax base and maintain a level playing

field.

20.

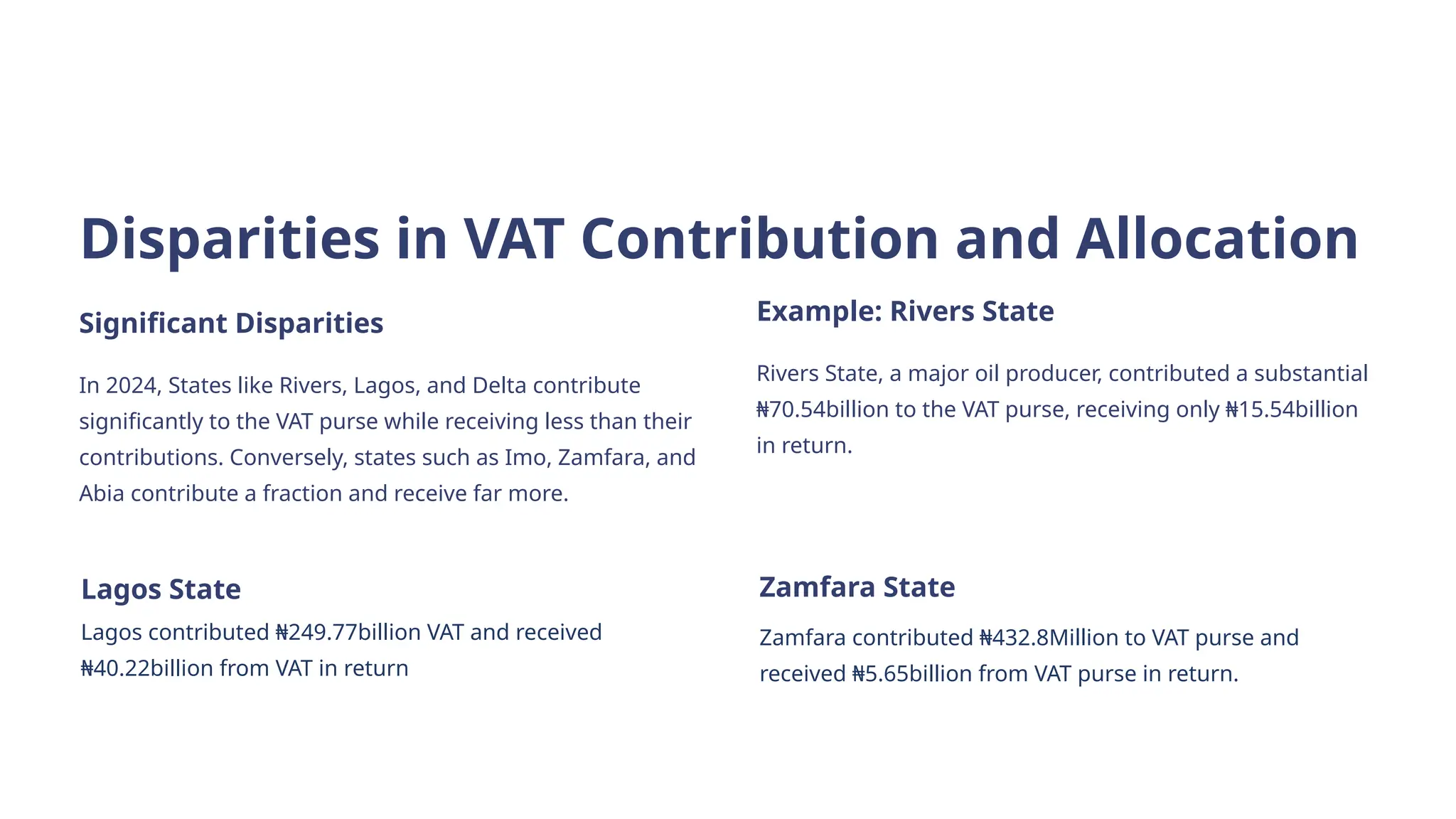

Disparities in VATContribution and Allocation

Significant Disparities

In 2024, States like Rivers, Lagos, and Delta contribute

significantly to the VAT purse while receiving less than their

contributions. Conversely, states such as Imo, Zamfara, and

Abia contribute a fraction and receive far more.

Example: Rivers State

Rivers State, a major oil producer, contributed a substantial

₦70.54billion to the VAT purse, receiving only ₦15.54billion

in return.

Lagos State

Lagos contributed ₦249.77billion VAT and received

₦40.22billion from VAT in return

Zamfara State

Zamfara contributed ₦432.8Million to VAT purse and

received ₦5.65billion from VAT purse in return.

21.

21

Impact on MSMEsand Startups

1 Reduced Compliance

Burden

Simplified regimes, such as

turnover-based taxation,

can ease the compliance

process for businesses with

limited financial expertise.

2 Cost Savings

Tax incentives for startups

can lower initial operating

costs, enabling them to

allocate resources toward

growth and innovation.

3 Encouragement of Formalization

Reduced rates and streamlined filing processes may incentivize

informal businesses to register and comply with tax laws.

4

Increased Access to

Financing

Formalized businesses with

better tax records are more

likely to attract loans and

investments, boosting

growth prospects

5 Technology Adoption

Encouraging digital tax

filing may promote broader

adoption of digital tools,

improving overall business

efficiency

22.

Implications of NewTax Laws

for Individuals and Businesses

1 Personal Income Tax

(PIT)

Applies to individuals with

progressive tax rates from 7% to

24%, depending on income.

Those earning below ₦1 million

annually may be exempt under

recent reforms.

2 Pay-As-You-Earn (PAYE)

Tax

Employers deduct income tax

from employees’ salaries.

Individuals earning less than

₦30,000 per month are often

exempt in some states.

3 Capital Gains Tax (CGT)

Individuals are subject to 10% CGT on gains from the disposal of chargeable

assets. Exemptions apply if proceeds are reinvested in another home.

23.

Tax Provisions forBusinesses in Nigeria

Companies Income Tax (CIT)

Applies to registered companies, excluding oil and gas.

Small businesses with turnover below ₦25 million are

exempt from CIT. Tax-exempt profits apply to priority

sectors for up to five years.

Value Added Tax (VAT)

Businesses collect 7.5% VAT on taxable goods and services.

Small businesses with turnover below ₦25 million are

exempt from VAT registration. VAT-exempt businesses

include those in health, education, and humanitarian

services.

24.

Personal Income Tax(PIT)

Filing for Individuals

File Annual Tax Returns

Individuals and sole proprietors must file their annual tax returns

with the State Internal Revenue Service (SIRS) where they reside.

Deadline: March 31st

The deadline for filing is March 31st of each year.

Filing Process

Fill and submit an Annual Income Tax Return (Form A), providing

details of income, reliefs, and allowances claimed. Pay applicable

PIT based on the progressive tax rate (7% - 24%).

25.

Companies Income Tax(CIT) Filing

for LLCs and Corporations

1 File Annual CIT Returns

All registered companies must file their annual Companies Income Tax (CIT)

returns with the Federal Inland Revenue Service (FIRS).

2 Deadline

New companies must file within 18 months of incorporation or 6 months after

their first financial year-end. Existing companies must file within 6 months

after the end of the financial year.

3 Filing Process

Submit audited financial statements, declare total revenue, expenses, and

taxable profits. Pay CIT at applicable rates (0%, 20%, or 30%, based on

company size).

26.

How WHT AffectsSMEs &

Consultancy Firms

Cash Flow Impact

Consultancy businesses face a 5-

10% deduction from invoices.

SMEs may have revenue tied up in

WHT deductions until a tax credit

is claimed.

Tax Credit & Recovery

WHT is an advance tax payment;

businesses can claim the deducted

amount as a tax credit when filing

annual tax returns.

Compliance Requirement

SMEs and consultants must register for a Tax Identification Number (TIN) to

receive WHT credit notes.

27.

How VAT AffectsSMEs and Consultancy

Businesses

VAT Collection Obligation

VAT-registered SMEs and

consultants must charge 7.5% VAT

on invoices and file VAT returns

monthly.

1

VAT Input & Output Tax

Adjustment

Businesses can deduct VAT paid on

purchases (input VAT) from VAT

collected on sales (output VAT).

2

Impact on Business Pricing

VAT increases the cost of services

and goods, which can make small

businesses less competitive.

3

28.

Service Type WHTRate for Individuals (%) WHT Rate for Companies (%)

Professional / Consultancy Services 5% 10%

Rent (Commercial Property) 10% 10%

Advertising Services 5% 10%

Building and Construction 5% 5%

Supply of Goods 5% 5%

Applicable WHT Rates for

Consultancy Businesses & SMEs

Annual Turnover (₦) Tax Rate (%) Applicable to

Below 25 million 0% Small businesses

25 – 100 million 20% Medium-sized companies

Above 100 million 30% Large companies

CIT Rates

Annual Income (₦) Tax Rate (%)

First 300,000 7%

Next 300,000 11%

Next 500,000 15%

Next 500,000 19%

Next 1,600,000 21%

Above 3,200,000 24%

Personal Income Tax (PIT)

29.

Tax Type WHT(Withholding Tax) VAT (Value Added Tax)

Nature of Tax Advance income tax deduction Consumption tax on goods/services

Who Pays?

Deducted from payments made to

businesses

Collected from customers and

remitted to FIRS

Who Remits?

The client or contracting company

deducts and remits WHT

The SME or consultancy firm

collects and remits VAT

Effect on Cash Flow

Reduces upfront revenue (5-10%

withheld)

Increases cost of goods/services

(7.5% added to price)

Refundability Can be claimed as a tax credit

Excess VAT input can be refunded

or carried forward

Compliance

Requirement

Register for TIN, obtain WHT credit

notes, include WHT in tax returns

Register for VAT if turnover > 25

₦

million, file monthly returns

Penalties for Non-

Compliance

200% of tax due + interest

₦50,000 fine for late registration,

10% penalty for late remittance

Summary of WHT vs. VAT Impact on SMEs & Consultancy Firms

30.

Criteria Federal TaxesState Taxes Local Taxes

Authority

Federal Government

(FIRS/NRS, Customs)

State Government (SIRS)

Local Government

Authorities

Coverage Nationwide Within each state

Within each local

government area

Who Pays?

Businesses, federal

employees, corporations

Employees, self-

employed individuals,

property owners

Market traders, transport

operators, local residents

Common

Examples

CIT, VAT, PPT, WHT,

CGT

PIT, Property Tax,

Business Premises Tax

Tenement Rate, Market

Fees, Park Fees

Usage of

Revenue

National infrastructure,

defense, education,

healthcare

State-level projects like

schools, roads, hospitals

Local sanitation, waste

management, grassroots

development

Differences between Federal, State, and Local Government Taxes

31.

Criteria

PAYE

(Employees)

Self-Assessment (Self-

Employed)

Payroll Taxes(Employers

& Employees)

Who Pays?

Employer deducts

and remits

Individual calculates and

pays

Employers & Employees

Filing Frequency

Monthly (by the

10th)

Annually (by March

31st)

Monthly/Annually

Applicable To Salaried workers

Freelancers,

entrepreneurs, rental

earners

All employees & businesses

Penalties for Non-

Compliance

Employer fined +

interest

Taxpayer fined 50,000

₦

Employer fined & subject to

audits

Key Differences between PAYE, Self-Assessment, and Payroll Taxes

32.

Conclusion

The Nigerian taxsystem's reforms aim to enhance efficiency and broaden the tax base, but their impact on SMEs is a

concern. SMEs are vulnerable to financial and administrative burdens associated with tax compliance. Effective tax

administration should balance revenue generation with a business-friendly environment.

Policy adjustments, stakeholder engagement, and capacity-building are necessary to ensure tax reforms support SMEs.

By addressing these concerns, Nigeria can foster an inclusive economic landscape where taxation serves as a tool for

development rather than a constraint on business growth.

33.

Prof. Godwin EmmanuelOyedokun

Professor of Accounting & Financial Development

Lead City University, Ibadan, Nigeria

Principal Partner; Oyedokun Godwin Emmanuel & Co

(Accountants, Tax Practitioners & Forensic Auditors)

[email protected]; [email protected]

+2348033737184 & 2348055863944

![Get a Pinterest account in[ pvatopservice ]sell regular every day.docx](https://cdn.slidesharecdn.com/ss_thumbnails/getapinterestaccountinpvatopservicesellregulareveryday-251030182004-67b5ef9f-thumbnail.jpg?width=640&height=640&fit=bounds)

![Get a Pinterest account in[ pvatopservice ]sell regular every day.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/getapinterestaccountinpvatopservicesellregulareveryday-251030182003-d27b98a4-thumbnail.jpg?width=640&height=640&fit=bounds)