Download as PDF, PPTX

This document discusses how corporate agendas can stifle lean thinking and provides examples of lean leaders who changed corporate agendas. It explores the basic language of corporate agendas and six schools of thinking that hinder lean, such as short-term focus, either/or thinking, and disrespect for production staff. Case studies of lean leaders like Art Byrne and Dr. John Toussaint demonstrate how changing metrics and empowering staff can improve both profits and outcomes. The document advocates studying lean management systems and getting involved in discussions to help shift corporate priorities towards lean.

Introduction to lean and consulting expertise in organizational improvement.

Emphasis on financial aspects like margins, costs, and balanced scorecard for lean implementation.

Discussion on objectives, KPIs, targets, and initiatives for assessing business success.

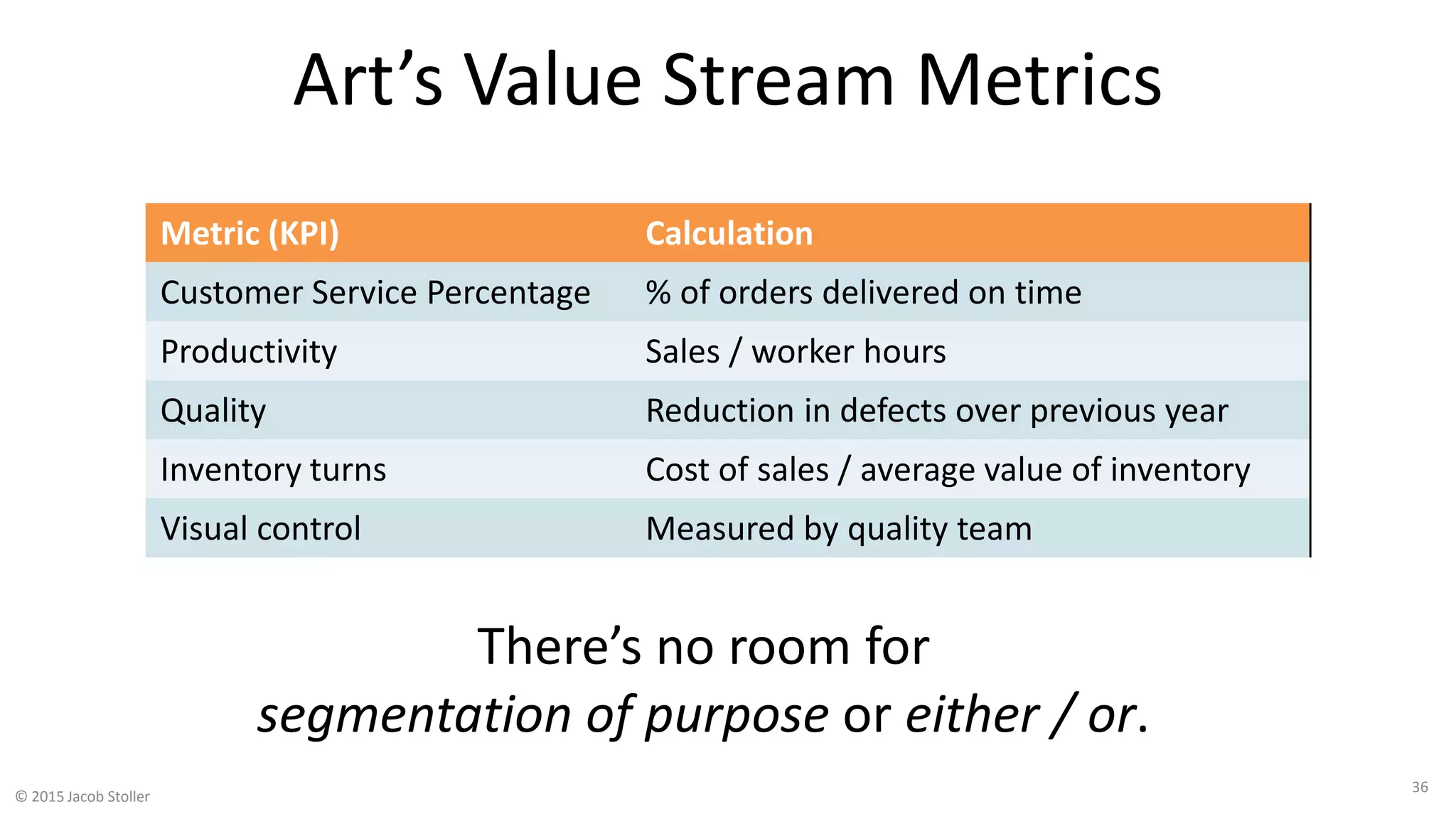

Identifying non-lean thinking challenges such as short-term focus and segmentation.

Explains pitfalls of GAAP accounting, automation faith, and focus on short term vs. long term.

Art Byrne's transformation at Wiremold emphasizing value in continuous improvements.

Dr. John Toussaint's approach to problem-solving in healthcare, emphasizing safety and standards.

Tom Everill's initiative showcasing profitability alongside employing people with disabilities.

Overview of lean gaining popularity, shifts in corporate agendas, and the call for dialogue.