Questions that weshould be able to answer

after this lecture

a) What is the central economic problem?

b) What does macroeconomics deal with?

c) What does microeconomics deal with?

d) What are three main categories of microeconomic

choice?

e) What does an opportunity cost mean?

f) What does a rational choice mean?

g) What does the production possibility curve show?

h) What are micro- and macroeconomic aspects of the

circular flow of goods and incomes?

3.

Economic decisions

• Decisionswe make about what to buy or what

job to do

• Decisions our government makes about how

much to tax us or what to spend those taxes

on.

4.

What do economistsstudy?

Economics is concerned with the following:

• The production of goods and services:

how much the economy produces, both in total and of individual items;

how much each firm or person produces;

what techniques of production are used;

how many people are employed.

• The consumption of goods and services:

how much the population as a whole spends (and how much it saves);

what the pattern of consumption is in the economy;

how much people buy of particular items;

what particular individuals choose to buy;

how people’s consumption is affected by prices, advertising, fashion and other

factors.

5.

Central economic problem

•What is the crucial ingredient that makes a

problem an economic one?

• This central economic problem is the problem of

scarcity.

• The point is that human wants are virtually

unlimited but there is a limited amount of

resources or factors of production

• Scarcity is the excess of human wants over what

can actually be produced to fulfil these wants.

6.

Scarcity of Factorsof Production

Factors of Production:

• Human resources: labour. The labour force is limited

both in number and in skills.

• Natural resources: land and raw materials. The world’s

land area is limited, as are its raw materials.

• Manufactured resources: capital. Capital consists of all

intermediate commodities. The world has a limited stock of

capital: a limited supply of factories, machines,

transportation and other equipment. The productivity of

capital is limited by the state of technology.

7.

Demand and Supply

•Relationship between Demand and Supply lie at the very centre

of economics.

• Demand is related to wants. Such wants are virtually boundless

• Supply, on the other hand, is related to resources. Such

resources are limited.

• Aggregate demand will need to be balanced against aggregate

supply. In other words, total spending in the economy should

balance total production.

• The demand and supply of cabbages should balance, and so

should the demand and supply of DVD recorders, cars and s.o.

• Economics studies how demand adjusts to available supplies,

and how supply adjusts to consumer demands.

8.

Macroeconomics

• Macroeconomics isconcerned with the economy as a whole. It

is thus concerned with aggregate demand and aggregate

supply.

• By ‘aggregate demand’ we mean the total amount of spending

in the economy, whether by consumers, by customers outside

the country for our exports, by the government, or by firms

when they buy capital equipment or stock up on raw materials.

• By ‘aggregate supply’ we mean the total national output of

goods and services.

• Macroeconomics is the branch of economics that studies

economic aggregates: e.g. the overall level of prices, output and

employment in the economy.

9.

Macroeconomics

• Because thingsare scarce, societies are concerned that

– their resources should be used as fully as possible, and that

– over time their national output should grow.

• If aggregate demand is too high relative to aggregate

supply, inflation and trade deficits are likely to result.

• If aggregate demand is too low relative to aggregate

supply, unemployment and recession may well result.

10.

Macroeconomic policy

Macroeconomic policy,therefore, tends to focus on

the balance of aggregate demand and aggregate

supply.

It can be demand-side policy, which seeks to influence

the level of spending in the economy. This in turn will

affect the level of production, prices and employment.

Or it can be supply-side policy. This is designed to

influence the level of production directly: for example,

by trying to create more incentives for firms to

innovate.

Microeconomics

Microeconomics is concernedwith the individual parts of

the economy. It is concerned with the demand and supply

of particular goods and services and resources: cars,

butter, clothes and haircuts; electricians, secretaries.

Microeconomics is the branch of economics that studies

individual units, e.g. households, firms and industries,

and the interrelationships between them

Microeconomics is concerned with the allocation of

scarce resources: with the answering of the what, how

and for whom questions.

13.

Three main categoriesof

microeconomic choice

• What goods and services are going to be produced

and in what quantities? How many cars, how much

wheat, etc. will be produced?

• How are things going to be produced? What resources

are going to be used and in what quantities? What

techniques of production are going to be adopted?

Will cars be produced by robots or by assembly line

workers?

• For whom are things going to be produced? In other

words, how will the nation’s income be distributed?

14.

Choice and opportunitycost

• The more food you choose to buy, the less money

you will have to spend on other goods.

• The more food a nation produces, the fewer

resources will there be for producing other goods.

• In other words, the production or consumption of

one thing involves the sacrifice of alternatives.

• This sacrifice of alternatives in the production (or

consumption) of a good is known as its

opportunity cost.

15.

Choice, opportunity cost,and rational choice

• If a nation devotes more of its resources to producing

manufactured goods, there will be less to devote to

the production of services or agricultural goods.

• What we give up in order to do something is known

as its opportunity cost.

• Opportunity cost is the cost of doing something

measured in terms of the best alternative forgone.

• Rational choice is weighing up the benefit of any

activity against its opportunity cost.

16.

Marginal costs andbenefits

• For example, the car firm will weigh up the marginal costs

and benefits of producing cars: in other words, it will

compare the costs and revenue of producing additional

cars. If additional cars add more to the firm’s revenue

than to its costs, it will be profitable to produce them.

• Rational decision making, then, involves weighing up the

marginal benefit and marginal cost of any activity. If the

marginal benefit exceeds the marginal cost, it is rational to

do the activity (or to do more of it). If the marginal cost

exceeds the marginal benefit, it is rational not to do it (or

to do less of it).

17.

Microeconomic objective: Efficiency

•Economic efficiency is thus achieved when each good is

produced at the minimum cost and where individual

people and firms get the maximum benefit from their

resources.

– Efficiency in production: A situation where firms are

producing the maximum output for a given amount of

inputs, or producing a given output at the least cost.

Producing any other way would cost more.

– Allocative efficiency: A situation where the current

combination of goods produced and sold gives the

maximum satisfaction for each consumer at their current

levels of income. Any other pattern of consumption would

make people feel worse off.

18.

Microeconomic objective: Equity

•Equity is where income is distributed in a way

that is considered to be fair or just. Note that

an equitable distribution is not the same as an

equal distribution and that different people

have different views on what is equitable.

19.

A production possibilitycurve

Production possibility curve – a curve showing all the possible

combinations of two goods that a country can produce within a

specified time period with all its resources fully and efficiently

employed.

20.

A production possibilitycurve

A nation devotes all its resources – land, labour and capital – to producing just two goods,

food and clothing. We measure units of food on the vertical axis and units of clothing on the

other. Thus the country, by devoting all its resources to producing food, could produce 8

million units of food but no clothing. At the other extreme, it could produce 7 million units

of clothing with no resources at all being used to produce food.

21.

A production possibilitycurve

Production cannot take place beyond the curve. For example, production is not possible at

point w: the nation does not have enough resources to do this.

A production possibility curve illustrates the microeconomic issues of choice and

opportunity cost. If the country chose to produce more clothing, it would have to sacrifice

the production of some food. This sacrifice of food is the opportunity cost of the extra

clothing.

22.

Increasing opportunity costs

Thecountry could move from point x to point y in Figure. In doing so it would be producing an extra 1

million units of clothing, but 1 million units less of food. Thus the opportunity cost of the 1 million extra

units of clothing would be the 1 million units of food forgone. The opportunity cost of the fifth million

units of clothing is 1 million units of food. The opportunity cost of the sixth million units of clothing is 2

million units of food. The reason for this is that different factors of production have different properties.

People have different skills; land differs in different parts of the country; raw materials differ one from

another; and so on. The production of more and more clothing will involve a growing marginal cost.

23.

Making a fulleruse of resources

The nation may thus be producing at a point inside the curve: for example, point v in Figure,

that is, the economy is producing less of both goods than it could possibly produce, either

because some resources are not being used (for example, workers may be unemployed), or

because it is not using the most efficient methods of production possible, or a combination

of the two. By using its resources to the full, however, the nation could move out on to the

curve: to point x or y, for example.

24.

Growth in theproduction possibilities (or potential output)

Over time, the production possibilities of a nation are likely to increase. Investment in

new plant and machinery will increase the stock of capital; new raw materials may be

discovered; technological advances are likely to take place; through education and

training, labour is likely to become more productive. This growth in potential output is

illustrated by an outward shift in the production possibility curve. This will then allow

actual output to increase: for example, from point x to point x in Figure.

′

25.

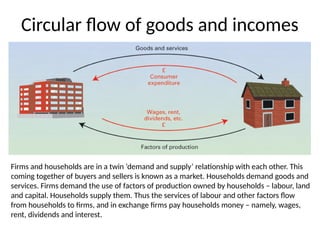

Circular flow ofgoods and incomes

Firms and households are in a twin ‘demand and supply’ relationship with each other. This

coming together of buyers and sellers is known as a market. Households demand goods and

services. Firms demand the use of factors of production owned by households – labour, land

and capital. Households supply them. Thus the services of labour and other factors flow

from households to firms, and in exchange firms pay households money – namely, wages,

rent, dividends and interest.

26.

Circular flow ofgoods and incomes

Microeconomics is concerned with the composition of the circular flow: what

combinations of goods make up the goods flow; how the various factors of

production are combined to produce these goods; for whom the wages, dividends,

rent and interest are paid out. Macroeconomics is concerned with the total size of

the flow and what causes it to expand and contract.

27.

Questions for discussing

Whichof the following are macroeconomic issues, which are

microeconomic ones?

(a) Inflation.

(b) Low wages in certain service industries.

(c) The rate of exchange between the pound and the euro.

(d) Why the price of cabbages fluctuates more than that of

cars.

(e) The rate of economic growth this year compared with last

year.

(f) The decline of traditional manufacturing industries.